MARKET OUTLOOK

Much of the uncertainties that raised caution in the market in 2023 are expected to persist into 2024, at least in the first half of the new year. Geopolitical tensions, macroeconomic headwinds, rising costs and high interest rates will continue to influence housing demand and risk appetite. Where interest rates are concerned, there is a likelihood that they may stabilise further, with some observers predicting the US Federal Reserve could start to trim rates from June 2024.

In addition, the Monetary Authority of Singapore has in October 2023 said that the Singapore economy is projected to improve gradually in the second half of 2024, and that Q3 2023 “likely marked the turning point in the slowdown”. Meanwhile, the labour market remains tight and unemployment rate is low which will help to support the housing market.

Going by recent primary market sales activity and bids for government land tenders, it appears that the residential property market remains relatively resilient, and that home buyers and developers are generally still confident about prospects in the housing market. In particular, the robust demand for well-located projects such as The Reserve Residences, Watten House, and J’den – suggests that the market still has ample liquidity to be deployed when highly attractive developments become available.

Collectively, three rounds of property cooling measures from December 2021 have helped to slow the momentum of price growth in both the private and public housing segments. In particular, the doubling of the additional buyer’s stamp duty (ABSD) rates on foreigners for home purchase to 60% from end-April 2023 has blunt foreign investment interest. To this end, developers will have to increasingly rely on the local market (Singaporean and Singapore permanent resident buyers) to drive project sales, especially in the Core Central Region which tends to see more foreign demand.

Over in the public housing segment, the effects of the cooling measures in September 2022 and the ramping up of new flat supply via the HDB’s Build-to-Order (BTO) exercises have moderated price growth in the HDB resale market. The HDB has committed to launch up to 100,000 BTO flats between 2021 and 2025, to meet current demand. In 2023, the housing board has launched 22,780 BTO flats.

One of the key things to look out for in the new year is the introduction of the Standard, Plus, and Prime HDB flat classification framework from the second half of 2024. The new framework will better reflect the locational attributes of BTO projects, with Plus and Prime flats – which will be in more attractive locations – being subjected to subsidy recovery, longer minimum occupation period of 10 years, and tighter conditions for resale and rental.

OVERVIEW

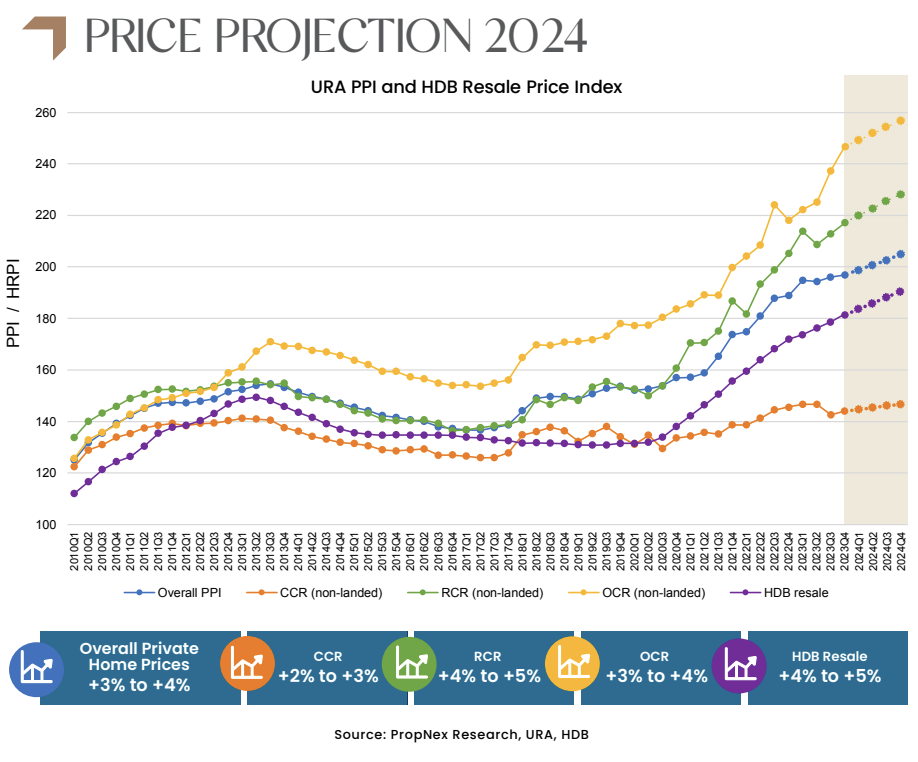

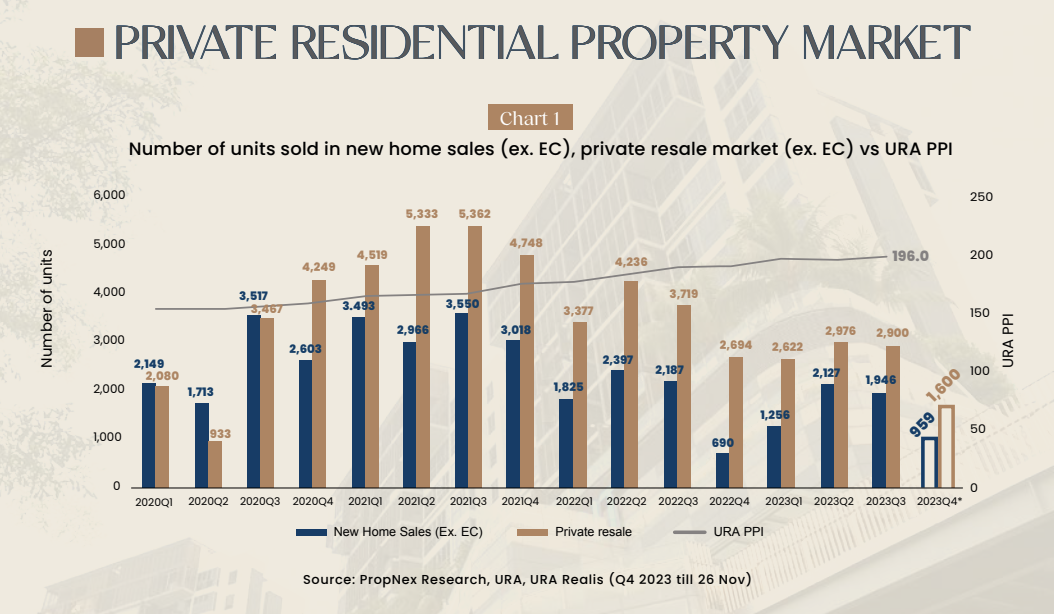

- PropNex projects that overall private home prices could grow by 3% to 4% for the full-year 2024 – slowing from what could be a 4% to 5% price increase in 2023. Firm land prices, rising construction costs, elevated interest rates, and new rules on gross floor area definitions will put upside pressure on prices. As at end of Q3 2023, the URA property price index has risen by a cumulative 3.9% in the first nine months of the year. As prices start to peak and cooling measures bite, the transaction volumes have also moderated in 2023 (see Chart 1).

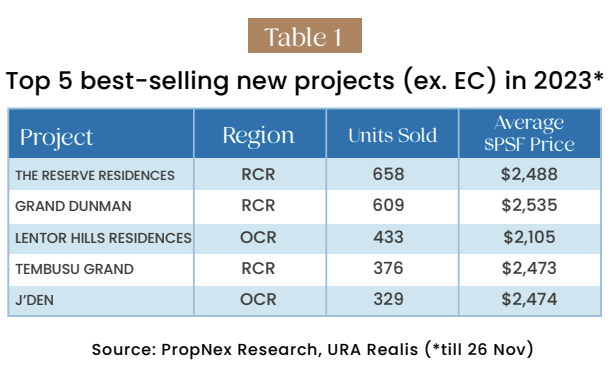

- Several projects launched in 2023 have set a new benchmark price in their respective planning area/segment. They included J’den (one of the best-sellers in 2023; see Table 1) which fetched an average price of $2,474 psf, TMW Maxwell which transacted new units at an average price of $3,348 psf, and Altura EC, where the average price touched a new high for ECs at $1,474 psf.

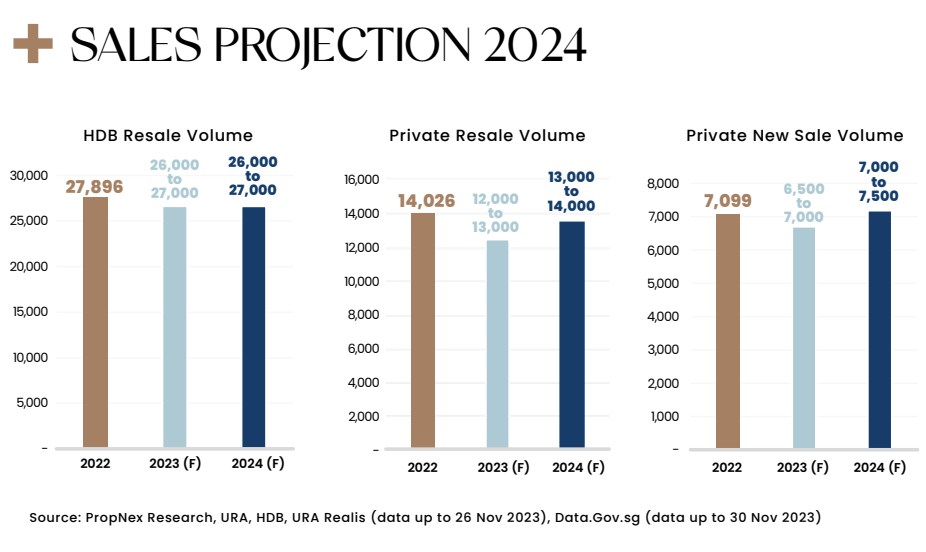

- New private home sales (ex. EC) look set to underperform the 7,099 units sold in 2022. As at 26 November 2023, developers have sold about 6,290 new units (ex. EC). PropNex expects 6,500 to 7,000 new homes to be transacted in 2023.

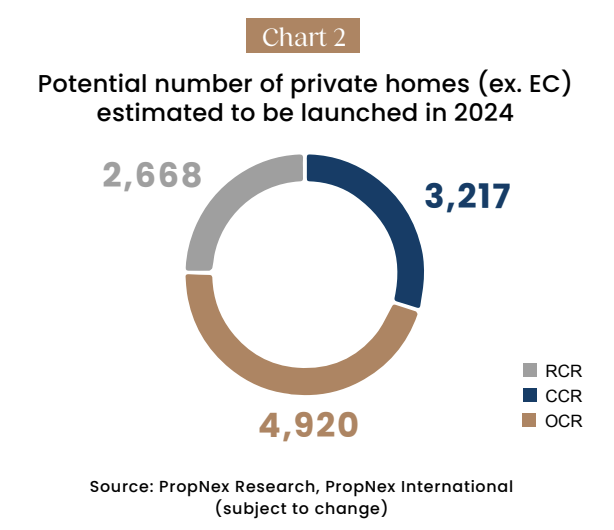

- Based on PropNex’s estimates, more than 30 projects (ex. EC) with over 10,000 residential units could potentially hit the market in 2024 (see Chart 2), with the Outside Central Region (OCR) accounting for nearly 46% of the supply.

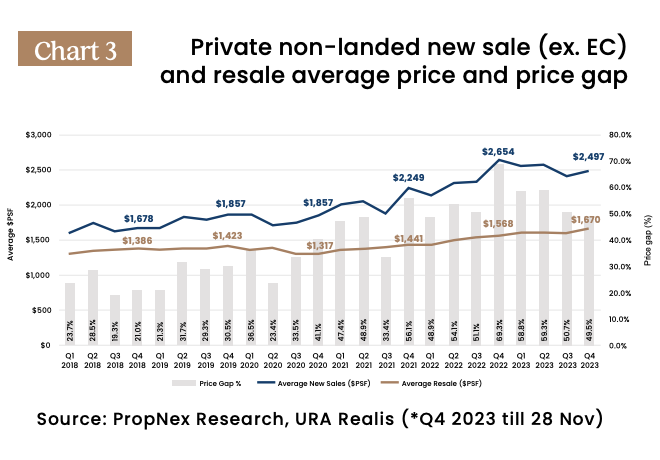

- In 2024, PropNex anticipates home sales to remain relatively stable with developers’ sales coming in at around 7,000 to 7,500 units (ex. EC), while the number of private homes resold may range from 13,000 to 14,000. The demand for resale properties is expected to remain stable amid their more affordable prices compared with new launches, with the average price gap at nearly 50% in Q4 2023 (see Chart 3).

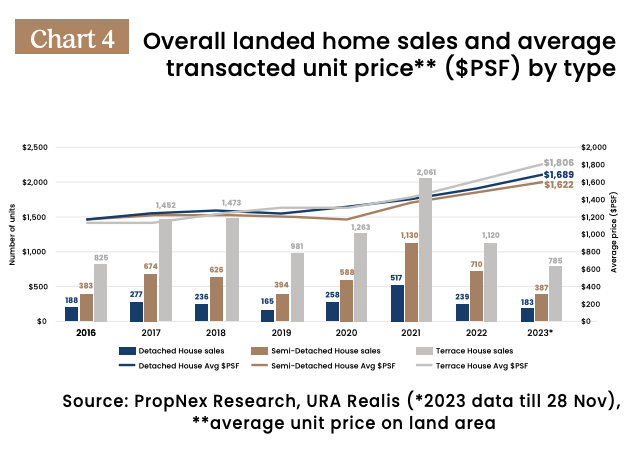

- On landed homes specifically, PropNex expects this segment to continue to experience slower sales due to the modest economic outlook and uncertainties in the market. However, landed home prices are still projected to be resilient in the near-term, as owners of such properties have substantial financial holding power and are not in a hurry to sell. Transactions of landed homes have been tepid in 2023, but the average unit prices on land area have generally held up in view of the scarce supply of such properties in Singapore (see Chart 4). The ABSD rate hikes for foreigners and investors are not likely to impact the landed homes market severely as these houses are predominantly purchased by Singaporeans and usually for own-stay

HDB Resale Market

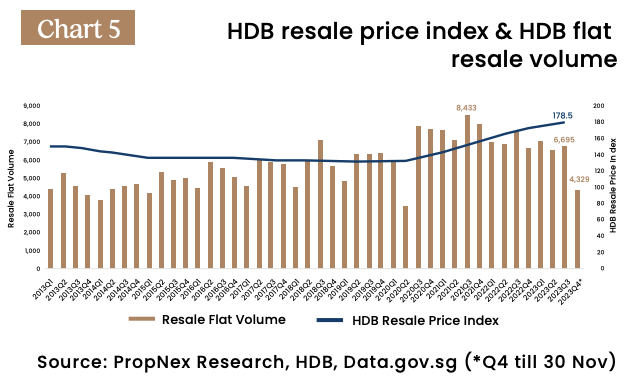

- The HDB resale market continued to power on in 2023, albeit losing some momentum from the prior two years. The HDB resale price index climbed by 1.3% QOQ (178.5 pts) in Q3 2023 and has reached a new peak (Chart 5). Overall HDB resale prices grew by a cumulative 3.8% in the first nine months of 2023, with PropNex projecting the full-year price growth to come in at around 5% in 2023. The price increase came amid a slight moderation transaction volume, as the ramping up of BTO supply could have funnelled some demand from the resale market.

- As of 30 November, about 24,500 resale HDB flats have changed hands in 2023 – with the full-year total likely to come in below the 27,896 flats resold in 2022.

- In 2024, PropNex expects HDB resale prices to climb at a more measured pace of 4% to 5% – in what could be the slowest year of price increase since 2020 where resale prices rose by 5%, and 2021 and 2022 where resale values surged by 12.7% and 10.4% respectively.

- Meanwhile, HDB resale volume could hover at around 26,000 to 27,000 units in 2024 – relatively on par with the sales in recent years. With the significant increase in BTO flat supply, elevated resale prices, and effects of the September 2021 cooling measures, it could be sometime before the market repeat the feat of the robust sales seen in 2021, where more than 31,000 flats were resold.

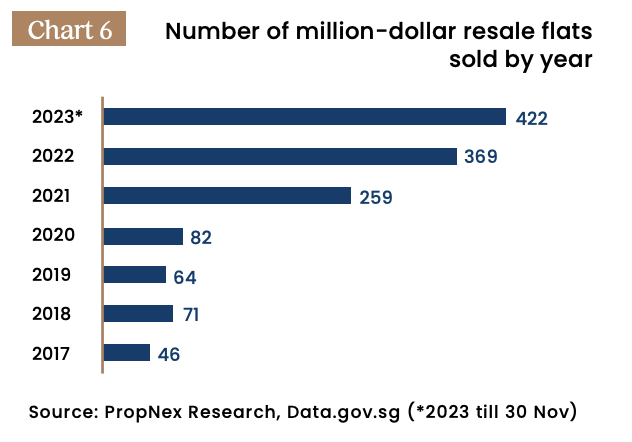

- The number of resale flats resold for at least $1 million came in at 422 units as at 30 November 2023 (see Chart 6) – already 14% higher than the record 369 units transacted in the whole of 2022.

- PropNex expects the number of million-dollar HDB flat transactions should remain elevated in 2024, as many buyers perceive these units which are frequently bestowed with desirable and unique attributes to offer bang for the buck, in view of the pricey private homes in the same location.

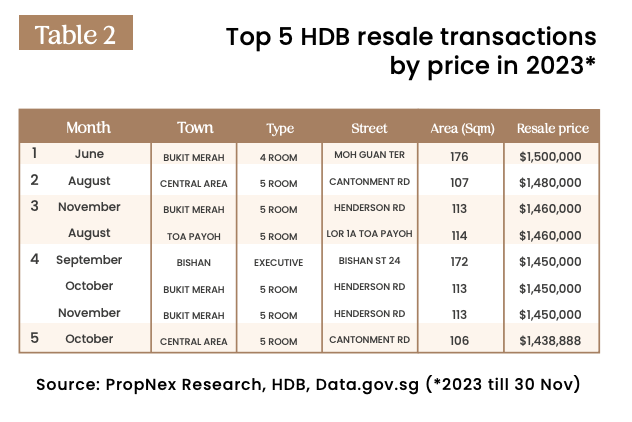

- Apart from rewriting the transaction volume of million-dollar resale flats, the prices of such flats also continued to move up. In June 2023, a large 176-sq m adjoined flat in Moh Guan Terrace in Bukit Merah became the most expensive resale flat ever transacted when it was sold for $1.5 million (see Table 2).

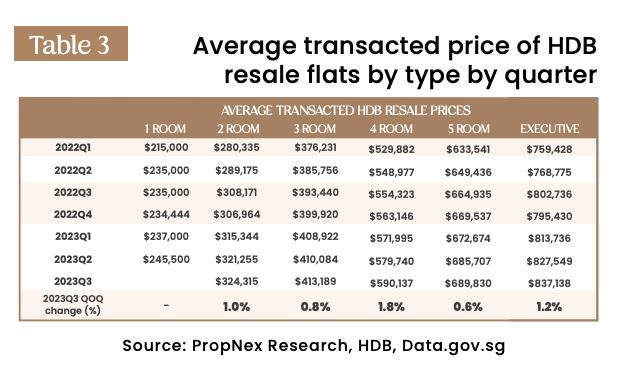

- By flat type, 4-room resale flats led average price growth in Q3 2023 – rising by 1.8% over the previous quarter. This was followed by executive flats and 2-room flats (see Table 3). Meanwhile, the average resale price of 3-room flats crossed the $400,000-mark in Q1 2023 and has stayed above that level since.

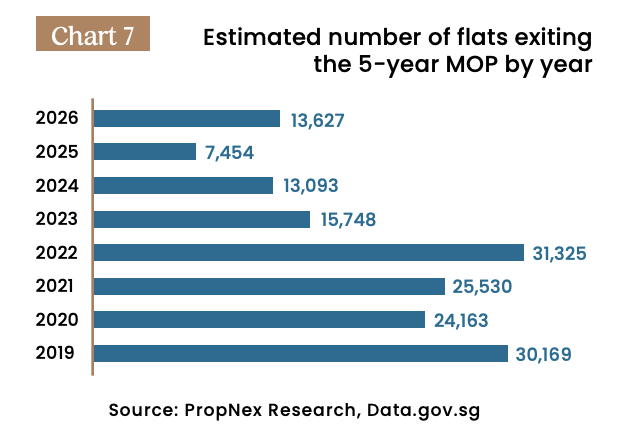

- Based on completion status of HDB projects, PropNex estimates that 13,093 HDB flats (see Chart 7) could potentially exit their respective 5-year minimum occupation period (MOP) in 2024, with Sembawang, Sengkang, Tampines, and Toa Payoh accounting for about 61% of the total. With fewer flats slated to exit the 5-year MOP in 2024, this could impact the resale stock available on the market. However, this could be supplemented by HDB upgraders who are seeking to sell their flats upon receiving keys to their newly completed homes.

- From the second half of 2024, new flats will be classified under a new “Standard, Plus, and Prime” framework, with the latter two categories subjected to a longer MOP and stricter resale/rental conditions. While the new framework will not affect existing flats, it is possible that some prospective buyers could be put off by the tighter restrictions for the Plus and Prime flats in choice locations (such as near town centres and the MRT station), and may decide to purchase resale flats nearby – this could then push up resale prices, depending on the lease balance and condition of the resale units.

Residential Leasing Market

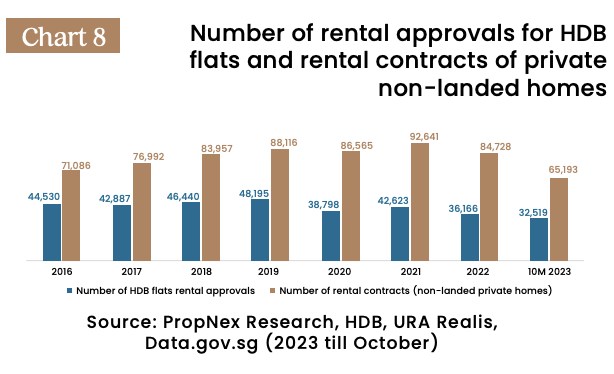

- The residential rental market was more subdued in 2023. An estimated more than 65,190 non-landed private home rental contracts were inked in the first 10 months of 2023 and it looks likely that the total rental volume in 2023 will underperform that of the previous year, where 84,728 rental deals were done (see Chart 8). Meanwhile, more than 32,500 HDB flats were estimated to have been leased in 10M 2023, and PropNex expects the total leasing volume in full-year 2023 to surpass the 36,166 rental approvals in 2022.

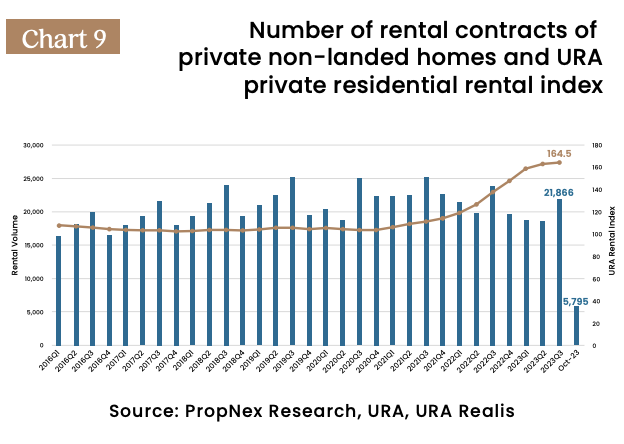

The robust growth in private home rentals, particularly in 2022 could have diverted some budget-conscious tenants to the HDB leasing market. Based on the URA private residential rental index (see Chart 9), rental rates have climbed by a cumulative 11.1% in the first nine months of 2023, following a 29.7% surge in rents in 2022. As rents crept higher, there may be rental price resistance among tenants leading to more muted leasing transactions.

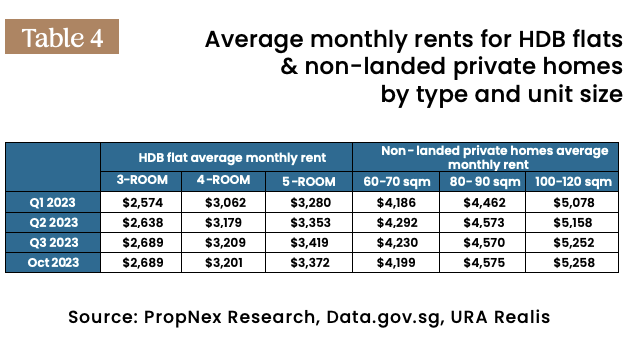

- In view of the firm private home rentals, some tenants could have sought cheaper options in the HDB leasing market (refer to Table 4 for average rentals comparison).

- PropNex expects private home rentals to rise by 11% to 12% in 2023, and possibly grow by 6% to 8% in 2024. With oncoming supply completions, some locations may see more readily available rental stock and this could potentially give tenants more bargaining power.

- As more new projects are completed, some tenants may not need to lease anymore, having received keys to their new homes. This could affect the number of lease renewals in the year. The URA expects 9,875 private homes and 2,157 ECs to be completed in 2024.

- Generally, leasing demand could still be supported by various segments: expatriates working in Singapore; international students; locals seeking to rent a larger home; those waiting for their new homes to be completed; private home down-graders waiting out the 15-month period before buying an HDB resale flat; as well as single-person households moving out to live on their own for greater privacy.

- That being said, leasing transactions could be sluggish as landlords may take time to review their asking rents, and a potential mismatch in rental expectations between landlords and tenants could slow rental transactions.

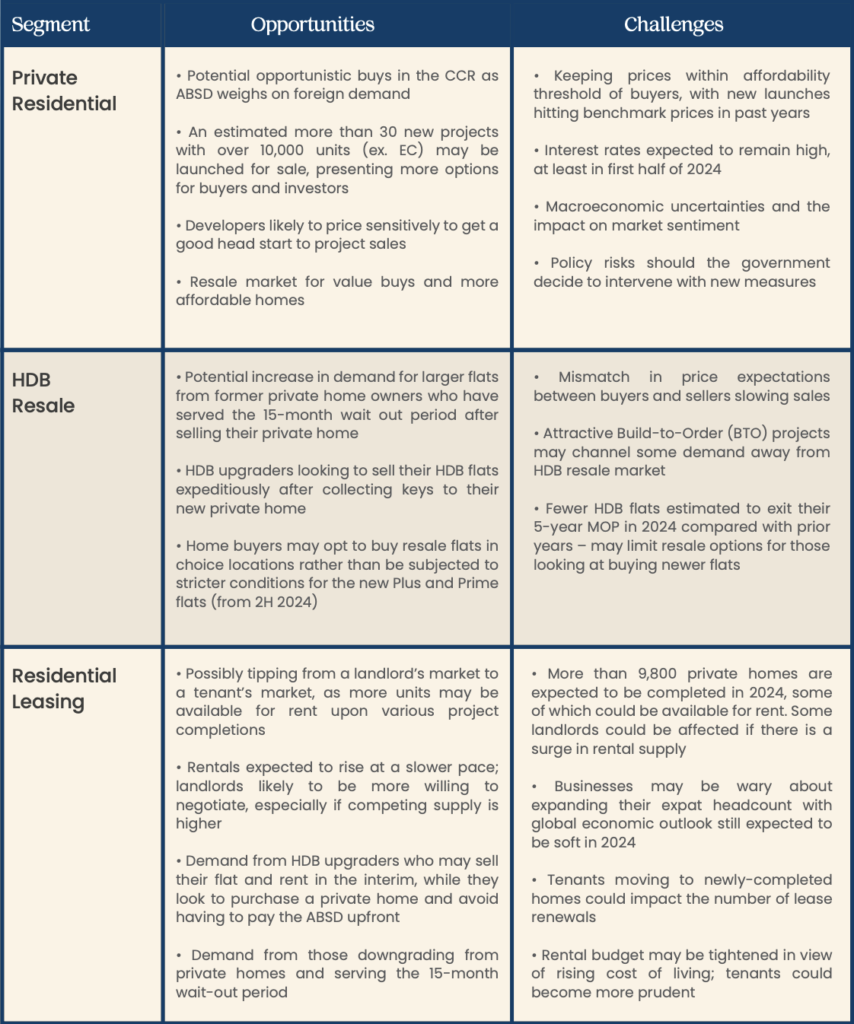

At a Glance:

2024 Opportunities & Challenges